Tony Meier | Windermere Real Estate | 37 Years Experience | 788 Closed Eastside Sales

Audio version here:

[audio mp3="https://eastsidehomes.com/wp-content/uploads/eastside_market_update_april_22_2026.mp3"][/audio]

Spring break has wound down across King and Snohomish County school districts and this week's data reflects a more normal operating environment. Buyers are back, inventory is still climbing, and the underlying market dynamics that defined March continue to hold.

If we can help you think through what this means for your move, we are here. Tony Meier & Team — Windermere Real Estate / NE, Kirkland, WA

📌 WHAT'S COVERED THIS WEEK

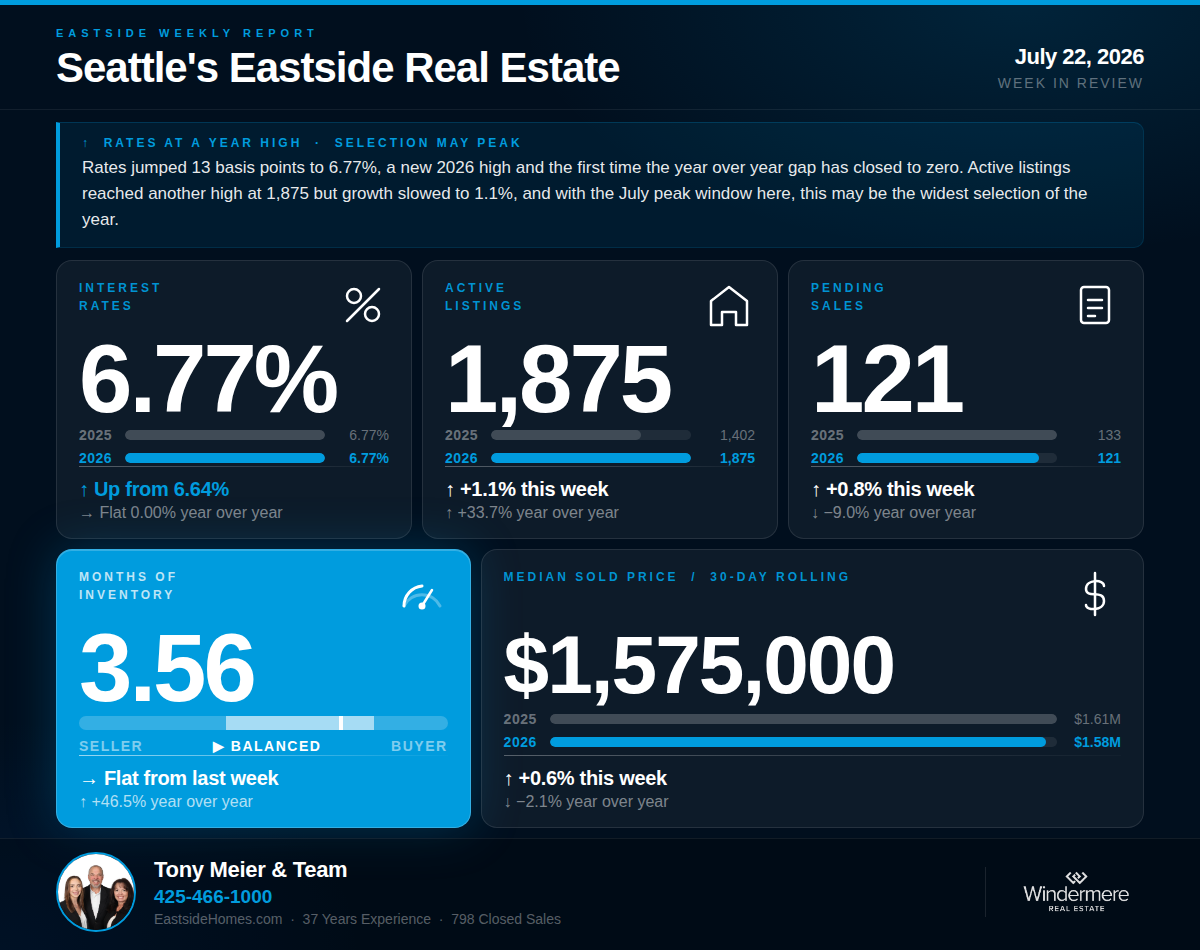

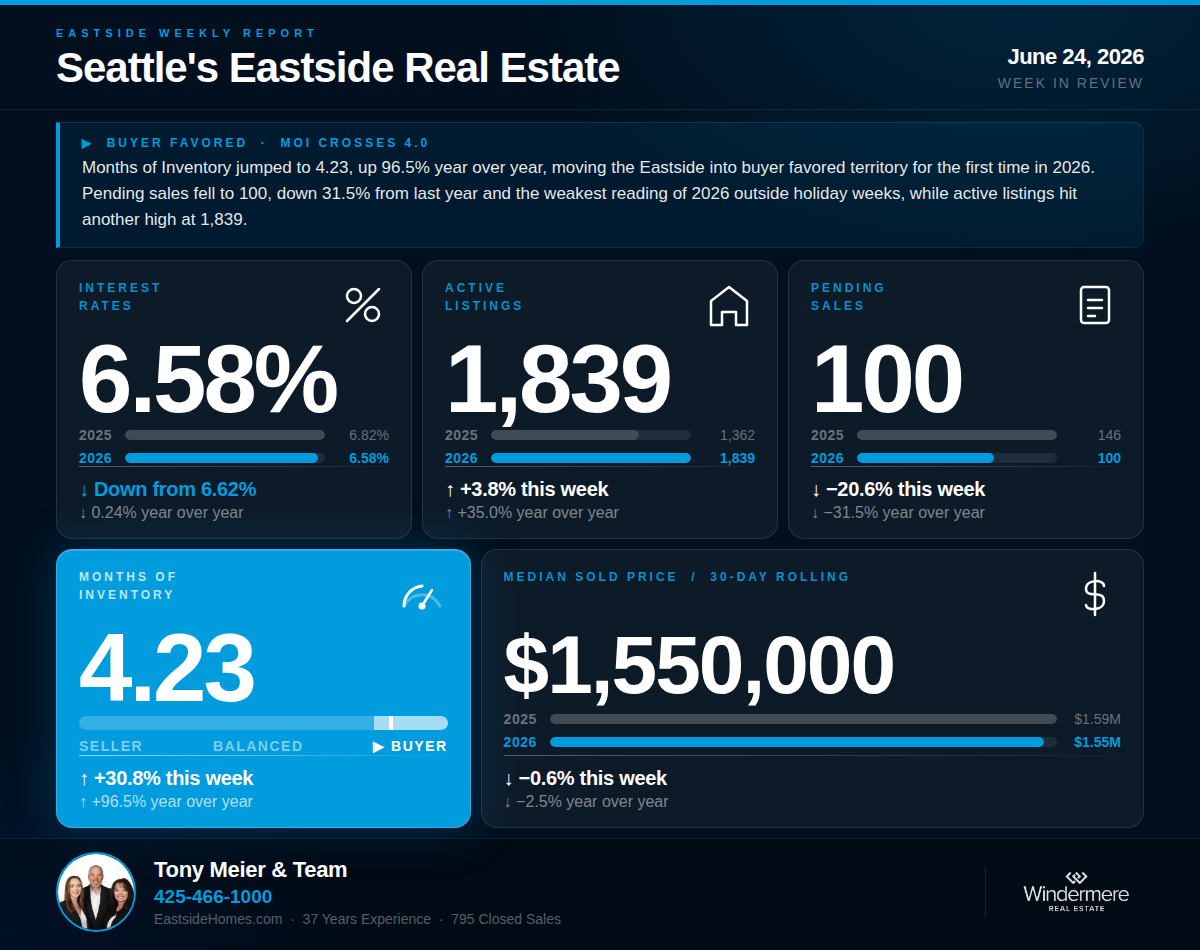

💰 INTEREST RATES — 6.32% | → Flat from last week | ↓ Down 0.66% year over year

Rates held steady at 6.32% this week — unchanged from last week and now down 0.66% compared to this same time one year ago. The year-over-year comparison has become a genuine tailwind for buyers. Rates currently sit 0.33 points above pre-conflict levels — the partial recovery from the peak spike continues to hold.🏡 ACTIVE LISTINGS — 1,314 | ↑ Up 5.5% from last week | ↑ Up 52.1% year over year

Active listings reached 1,314 this week — another 2026 high and up 52.1% from the 864 homes on the market during the comparable week in 2025. The seasonal inventory build is continuing, and with spring break fully behind us, new listings are coming to market at a pace consistent with the broader trend we have tracked since February.📝 PENDING SALES — 125 | ↓ Essentially flat from last week's 128 | ↑ Up 15.7% year over year

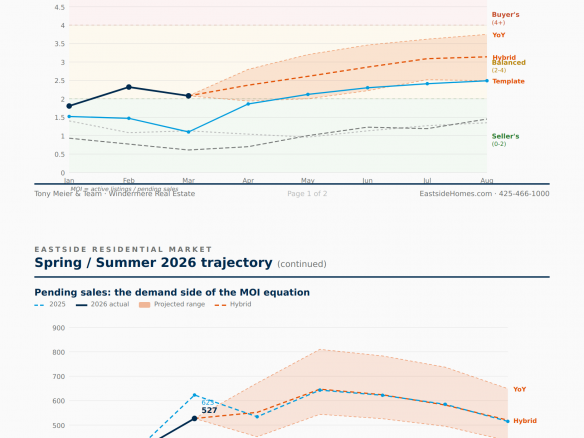

Pending sales came in at 125 — essentially holding the post-spring-break rebound level from last week, and up 15.7% compared to the 108 contracts written during the same week in 2025. Two consecutive weeks of pending sales above 120 confirm that buyers are active and engaged. Demand is present — it is inventory growth that is outpacing it.📦 MONTHS OF INVENTORY — 2.43 | ↑ Up 8.1% from last week's 2.24 | ↑ Up 31.4% year over year

MOI settled at 2.43 this week — up modestly from last week's 2.24 as inventory continued to grow faster than pending sales. At 2.43, MOI remains solidly in balanced market territory, defined locally as 2 to 4 months, and is 31.4% above the 1.85 recorded during the comparable week in 2025. This is the clearest post-spring-break read we have had on where the market is actually operating, and it confirms the balanced conditions that have defined 2026 since early March.🏠 MEDIAN SOLD PRICE (Rolling 30-Day) — $1,515,000 | ↓ Down 1.5% from last week | ↓ Down 10.9% year over year

The 30-day median eased slightly to $1,515,000 — down 1.5% from last week and now 10.9% below the $1,700,000 recorded at this same point in 2025. The weekly closed median of $1,500,000 is consistent with that picture. Prices are not collapsing, but the year-over-year gap has widened to nearly 11% and shows no sign of closing in the near term.🔍 THE BIG PICTURE — WHAT THIS ALL MEANS

With spring break behind us, this week provides the clearest picture of where the April market is genuinely operating. The takeaway is consistent with what the data has shown since March: buyers are active, inventory is running well above recent spring averages, and MOI is at its highest seasonal level since 2011. Two consecutive weeks of pending sales above 120 confirm demand has not evaporated — it is simply navigating a market with materially more supply than it has seen at this time of year in over a decade. For sellers, the margin for error on pricing remains narrow. For buyers, the leverage that comes with balanced conditions is real and present.🏠 FOR SELLERS

With 52.1% more competition on the market than a year ago, pricing discipline is the single most important decision you will make. Homes priced accurately against today's comparable sales — not 2025 peaks, and not even the partial recovery readings from January and February 2026 — are still selling well, while overpriced listings are sitting longer and often requiring reductions that erode both value and negotiating position. We have done extensive analysis on exactly what this market shift means for sellers in each Eastside sub-market — if you are considering a move, we would welcome the opportunity to walk you through what the data shows for your specific area and home.🔑 FOR BUYERS

Buyers today have more negotiating leverage for this time of year — spring — than at any point since 2011. Two consecutive weeks of strong pending numbers confirm that well-priced homes are still attracting offers. More choices, more time to conduct proper due diligence, and more room for thoughtful negotiation than buyers have experienced in years — but arriving pre-approved and prepared remains essential in a market where accurately priced homes are still moving.If we can help you think through what this means for your move, we are here. Tony Meier & Team — Windermere Real Estate / NE, Kirkland, WA