Click the images below to download your free copy!

Hosted by Tony Meier & Team - Windermere Real Estate/NE

Click the images below to download your free copy!

Every year around this time, many homeowners begin the process of preparing their homes in case of extreme winter weather. Some others skip winter all together by escaping to their vacation homes in a warmer climate.

For those homeowners staying at their first residence, AccuWeather warns:

“The late-week cold shot should fade next week, but this is a warning shot for winter’s return late in the month and early February.”

Given this, it’s time to go and stock up on winter weather supplies! However, if you’re tired of shoveling snow and dealing with the cold weather, maybe it’s time to consider obtaining a vacation home!

According to the Investment & Vacation Home Buyers 2018 Report by NAR:

“72% of vacation property owners and 71% of investment property owners believe now is a good time to buy.”

It’s time to take advantage of the equity in your home. As the latest Equity Report from ATTOM Data Solutions stated:

“Nearly 14.5 million U.S. properties (are) equity rich — where the combined estimated amount of loans secured by the property was 50 percent or less of the property’s estimated market value — up by more than 433,000 from a year ago to a new high as far back as data is available, Q4 2013.

The 14.5 million equity rich properties in Q3 2018 represented 25.7 percent of all properties with a mortgage.”

This means that over a quarter of Americans who have a mortgage would be able to use some of their home equity to make a significant down payment toward a vacation home, and many are doing just that! According to the same report by NAR:

“33% of vacation buyers purchased in a beach area, 21% purchased on a lakefront, and 15% purchased a vacation home in the country.”

Many homeowners who are close to retirement will use some of their equity to purchase vacation homes, which may eventually become their permanent homes post-retirement!

If you are a homeowner looking to take advantage of your home equity by investing in a vacation home, let’s get together to discuss your options!

KIRKLAND, Washington (January 7, 2019) – December brought few surprises for real estate brokers in Western Washington with holidays, fluctuating interest rates, and volatility in consumer confidence contributing to slower activity. Several leaders from Northwest Multiple Listing Service described 2018 as a transition year for residential real estate.

New data from the MLS show inventory in its 23-county market area dipped below two months of supply for the first time since July. A year-over-year comparison of the number of new listings, pending sales, and closed sales show drops overall, while prices rose from the same month a year ago.

Member-brokers added 3,631 new listings of single family homes and condominiums during December (10.4 percent fewer than a year ago), boosting total active listings to 12,275, up from the year-ago volume of 8,553. Pending sales were down about 8.4 percent from twelve months ago (5,677 versus 6,198), and the volume of closed sales dropped nearly 16.6 percent (6,374 versus 7,642).

For 2018, members of Northwest MLS reported completing 92,555 transactions, which compares with 99,345 closed sales during 2017 for a drop of about 6.8 percent. The median price on last year’s closed sales of single family homes and condominiums combined was $402,000, up $32,000 (8.64 percent) from 2017.

Commenting on inventory, declines in closed sales and the drop in month’s supply, MLS director Dick Beeson said, “There’s lots of speculation as to the reasons why. One thing for sure: this situation can make for a deliciously deceptive market for either buyers or sellers.” The veteran Realtor said buyers who are paying attention will find very good values and receptive sellers.

“Timing the interest rate market is beyond the capability of most everyone. Therefore, buyers should act now, act deliberately, act decisively, and act in conjunction with an experienced real estate professional,” advised Beeson, the principal managing broker at RE/MAX Northwest in Gig Harbor.

Brokers said many of last month’s buyers took advantage of the shifting market.

“Buyers in December were reaping the benefits of market-weary sellers who were willing to give up part of their bloated home equity to make a deal and move on,” reported John Deely, principal managing broker at Coldwell Banker Bain.

James Young, director of the Washington Center for Real Estate Research at the University of Washington, noted last month was a very different December from a year ago. “While active listings are up significantly (43.5 percent) from a year ago, interest rates have also gone up by over 80 basis points, meaning the typical mortgage repayment has increased by about 10 percent for those looking to buy. That limits spending power and stops buyers from bidding up for the house they want rather than the house they can afford.”

The 12,275 active listings in the MLS database at year end was down from November when inventory totaled 15,830 properties, and down from 2018’s peak of 19,526 listings at the end of September. Measured another way, there was 1.93 months of supply at the end of December, with four-to-six months typically considered to be a balanced market. A year ago there was only 1.12 months of supply. On a percentage basis, year-over-year inventory has climbed each month since May.

Five counties had less than two months of supply at year end, with Kitsap having the scarcest selection at only 1.48 months of supply. Other counties reporting less than two months of supply were Pierce (1.52), Snohomish (1.53), Thurston (1.58), and King (1.71). Brokers note some of the December shrinkage is seasonal since some sellers take their home off the market during the holidays.

Condo inventory surged, notably in King County which now has more than four times the number of condo listings than 12 months ago.

“We’re continuing to see a balancing of the market, yet it is still seller-leaning, driven by our region’s continued job formation and a lack of inventory,” observed Mike Grady, president and COO of Coldwell Banker Bain. “For all the talk of doom and gloom in real estate” he said his calculations show home values have increased at four times the rate of inflation since December 2014 when the “hot market” began.

Grady pointed to the gap between December’s closed sales (6,374) and the volume of new listings (3,631) to replenish supply. He expects more growth in inventory this year, “but still not to the level of a truly balanced market of five or so months of supply.” Grady also anticipates prices increases, “although not at the rate they have been. So, still a great time for both buyers and sellers to enter the market.”

Other industry leaders also described the market in terms of a transition or recovery.

Lennox Scott, chairman and CEO of John L. Scott Real Estate, said a favorable market is returning for home buyers in Seattle and the Eastside. “Improved affordability, with both lower interest rates and adjusted lower housing prices from the spring of 2018 will lead the way,” he stated, adding “Although unsold inventory of homes for sale is still considered a shortage, the larger number of unsold homes, combined with new listings, will moderate the price increases in the year ahead.”

“Last year was a recovery year,” said George Moorhead, who believes 2019 will mirror it in several ways. “Balancing inventory, moderate appreciation of home values, tempered buyer demand with rising interest rates and reduced tax incentives” are among his expectations. “Buyer affordability in 2019 will be based on perception of good value and mortgage interest rates,” suggested Moorhead, the designated broker and owner of Bentley Properties. “The looming feeling of a hard-hitting recession keeps many would-be homeowners on the sidelines, thinking ‘It is better to watch and wait’ even though economic factors point towards a continued healthy, yet moderate market.”

John Deely called 2018 “the transition year for the traditional Pacific Northwest 10-year market cycle.” The swing from a sellers’ market to a more balanced market was evident by the second quarter of 2018 as the absorption of new and standing inventory slowed due to a decrease in pending sales explained Deely, a member of the Northwest MLS board of directors.

Three factors contributed to the change, according to Deely. He listed accelerated and unsustainable home price growth, rising interest rates, and waning consumer confidence and sentiment as those factors, noting “The market is mimicking the strong recession recovery cycles of 2012 to 2014.”

“The year ended with more of a splutter than a bang as home price growth continued to slow in December,” stated OB Jacobi, president of Windermere Real Estate. “But it’s important to keep things in perspective,” he emphasized, saying 2018 was a very good year for Seattle-area home sales. “The shift we’re experiencing is only bringing us closer to a more balanced market. My crystal ball tells me this trend will continue in the coming year with home prices rising, but at a slower rate of around 5.5 percent.”

Young, from the Center for Real Estate Research, commented on activity moving away from core urban areas to outlying regions where prices are cheaper. Demand is pushing prices higher and shortening market time in several counties, he stated, naming Cowlitz, Lewis and Thurston, which all experienced year-over-year price gains of at least 12.4 percent.

“Regardless of what the news is saying about the Seattle market, at the end of the day, the Kitsap median home price is significantly lower than a home in King County,” said Frank Wilson, Kitsap regional manager and branch managing broker at John L. Scott Real Estate in Poulsbo. Northwest MLS data show the median price for homes and condos that sold last month in Kitsap County was $343,000, while in King County it was 74 percent higher ($597,000).

“This will be what keeps our inventory low due to the improved mobility between Colman Dock and Kingston, Bremerton, and eventually Port Orchard,” Wilson remarked. He noted the early success of the fast ferry on the Kingston run is leading to talks about adding more boats.

Wilson said Kitsap brokers report good traffic at open houses and multiple offers on correctly priced homes. “We’ve also seen prices of homes in the north end go up, as well as an increase in new construction in the area,” added Wilson, who is also a director at NWMLS.

Beeson also commented on the importance of pricing. “Sellers who recognize a market shift has occurred will price their homes accordingly and sell in a reasonable amount of time, 30 days or less – not one day.”

Young said buyers are very aware of the changing housing finance environment and are still active in the marketplace even if they are not as aggressive as they have been in the past. Mortgage applications are declining due to short-term uncertainty, he said, even though 30-year fixed rate mortgage interest rates are continuing to fall.

Moorhead echoed that thought. “Buyers are being much more methodical about their purchase with some taking as long as eight months before making their final decision,” he reported.

Jacobi believes 2019 will bring the continued resurgence of first-time buyers, especially millennials as they form new households, get married, and have children. “Although many of them will face significant obstacles to buying due to student debt, lack of down payments, and Seattle’s high-priced housing, this group is likely to buy more homes in 2019 than any other demographic,” Jacobi predicts.

Wilson characterized the seasonally slower December/early January period as “the calm before the storm,” noting the spring market usually brings a surge of buyers that surpass the increase in listings.

Every homeowner wants to make sure they maximize their financial reward when selling their home. But how do you guarantee that you receive the maximum value for your house?

Here are two keys to ensure that you get the highest price possible.

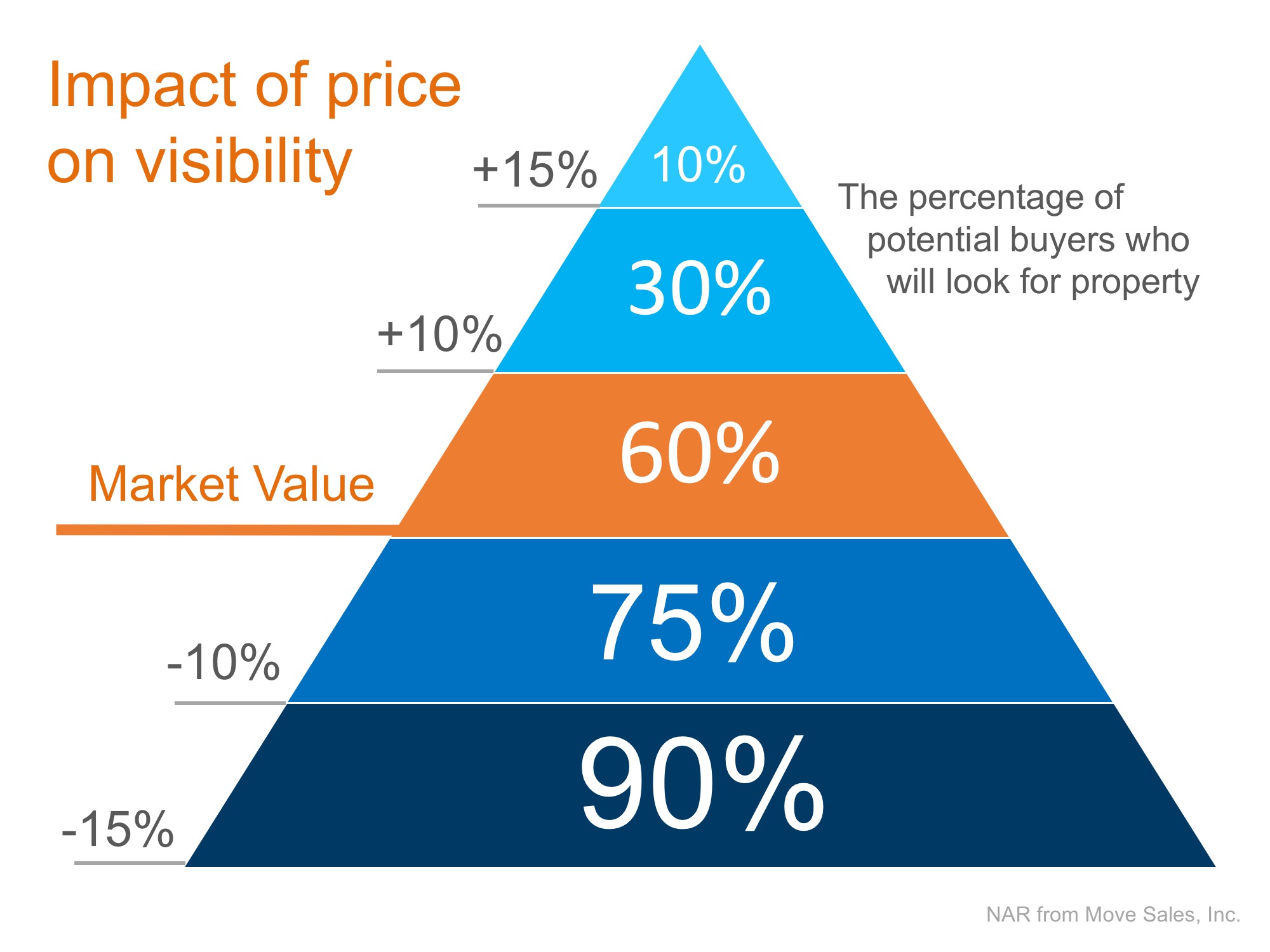

1. Price it a LITTLE LOW

This may seem counterintuitive, but let’s look at this concept for a moment. Many homeowners think that pricing their homes a little OVER market value will leave them with room for negotiation. In actuality, this just dramatically lessens the demand for your house (see chart below).

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price it so that demand for the home is maximized. By doing this, the seller will not be fighting with a buyer over the price but will instead have multiple buyers fighting with each other over the house.

HGTV gives this advice:

“First impressions are everything when selling your home. Studies have shown that the first two weeks on the market are the most crucial to your success. During these initial days, your home will be exposed to all active buyers.

If your price is perceived as too high, you will quickly lose this initial audience and find yourself relying only on the trickle of new buyers entering the market each day. Markets are dynamic, and your price has an expiration date. You have one chance to grab attention. Make sure your pricing helps you stand out on the shelf — in a positive way.”

2. Use a Real Estate Professional

This, too, may seem counterintuitive. The seller may believe that he or she will make more money without having to pay a real estate commission, but studies have shown that homes typically sell for more money when handled by a real estate professional.

Research by the National Association of Realtors in their 2018 Profile of Home Buyers and Sellers revealed that,

“the median selling price for all FSBO homes was $200,000 last year. However, homes that were sold with the assistance of an agent had a median selling price of $264,900 – nearly $65,000 more for the typical home sale.”

Price your house at or slightly below the current market value and hire a professional. This will guarantee that you maximize the money you get for your house.

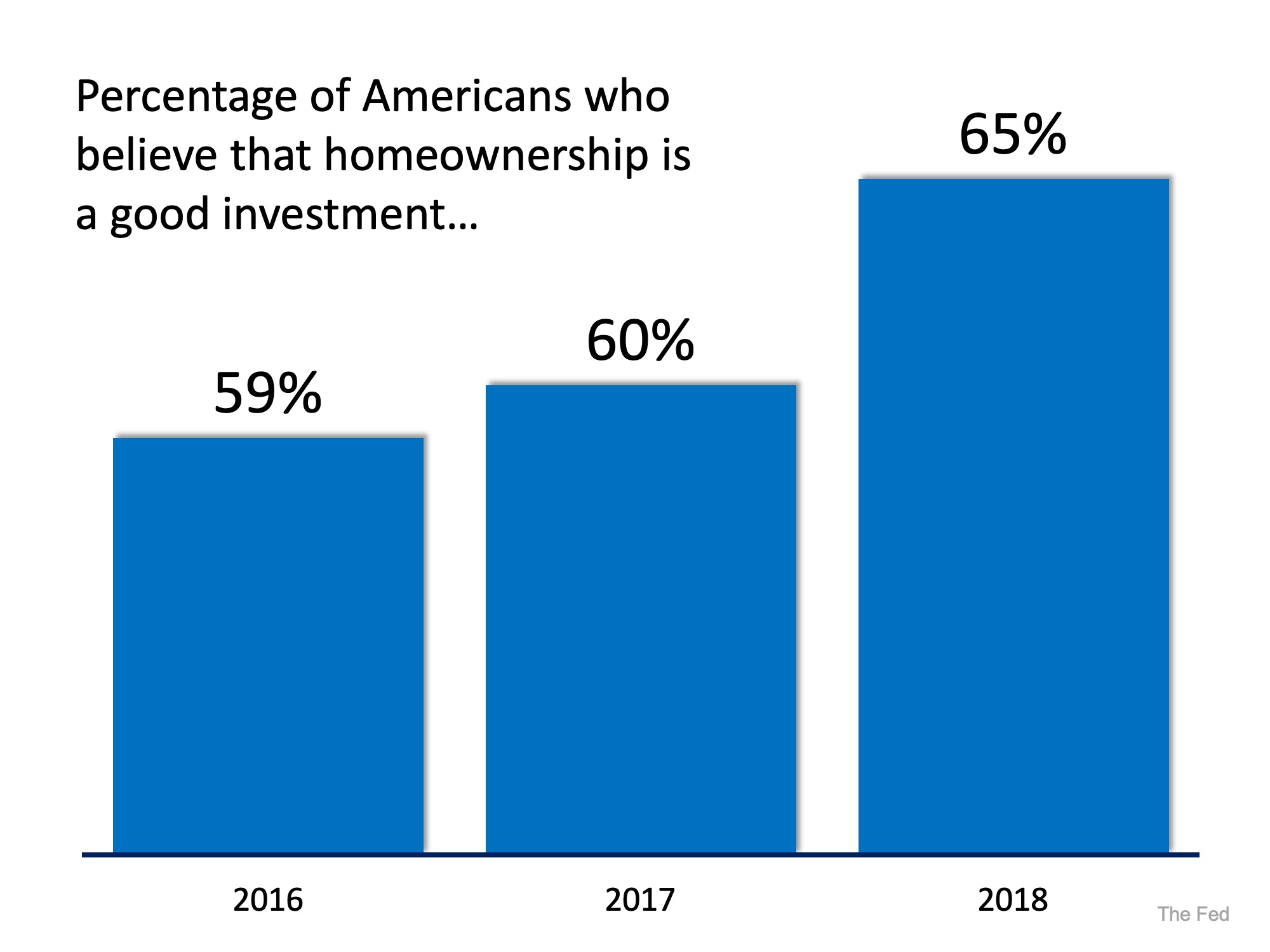

Following last year’s real estate market was like riding a rollercoaster. The market started off strong in 2018 and then softened before finishing with a mild flurry. However, one thing that did not waiver was America’s belief that owning a home makes sense from a financial standpoint.

An end-of-the-year survey by the Federal Reserve Bank’s Center for Microeconomic Data revealed that:

“The majority of households continue to view housing as a good financial investment.”

And that percentage has increased over the last three years.

Though there is some uncertainty as to how the real estate market will perform over the next twelve months, one thing remains very certain: America’s belief in homeownership.

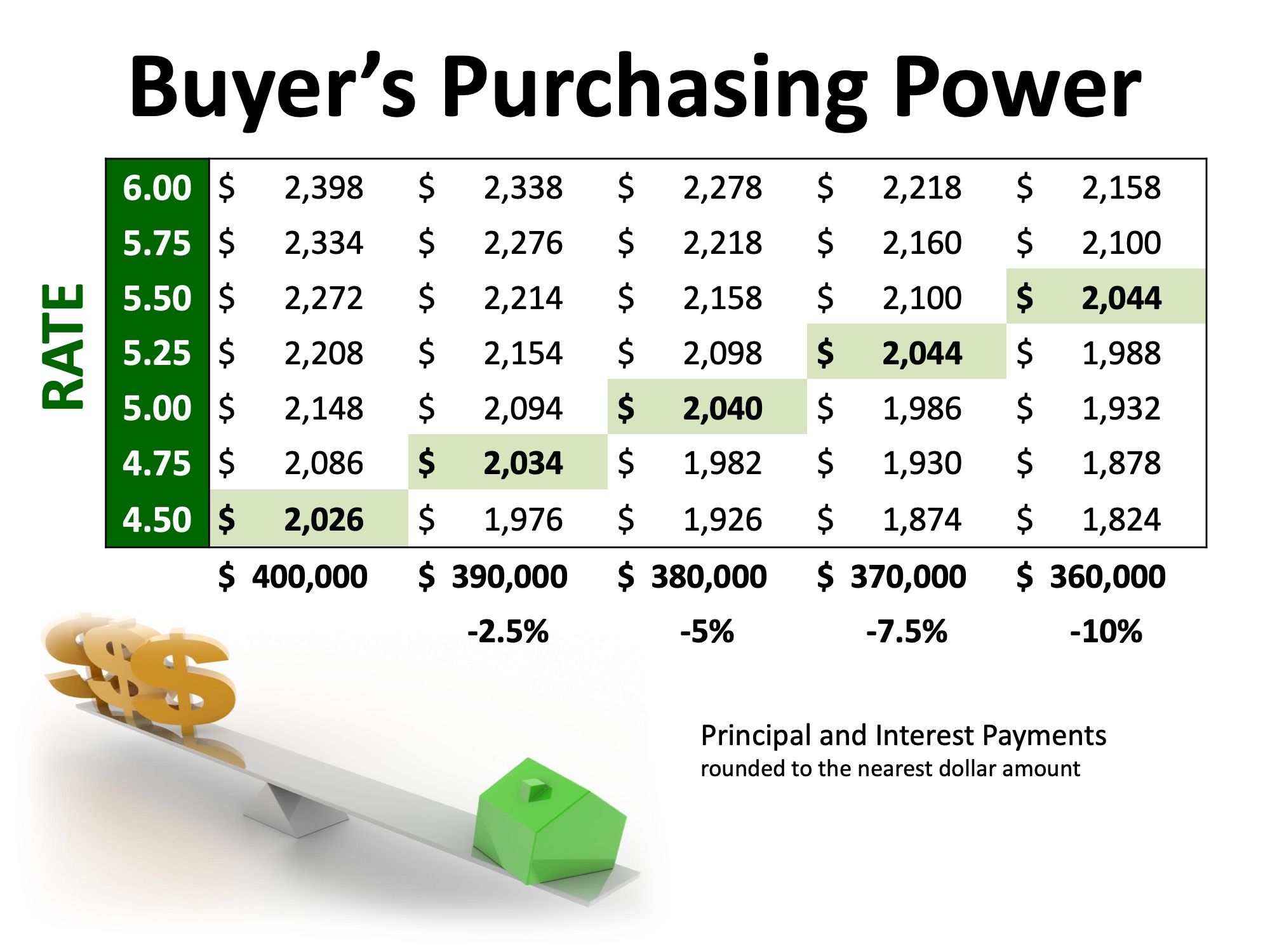

As we kick off the new year, many families have made resolutions to enter the housing market in 2019. Whether you are thinking of finally ditching your landlord and buying your first home or selling your starter house to move into your forever home, there are two pieces of the real estate puzzle you need to watch carefully: interest rates & inventory.

Mortgage interest rates had been on the rise for much of 2018, but they made a welcome reversal at the end of the year. According to Freddie Mac’s latest Primary Mortgage Market Survey, rates climbed to 4.94% in November before falling to 4.62% for a 30-year fixed rate mortgage last week. Despite the recent drop, interest rates are projected to reach 5% in 2019.

The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford to buy will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows the impact that rising interest rates would have if you planned to purchase a $400,000 home while keeping your principal and interest payments between $2,020-$2,050 a month.

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000).

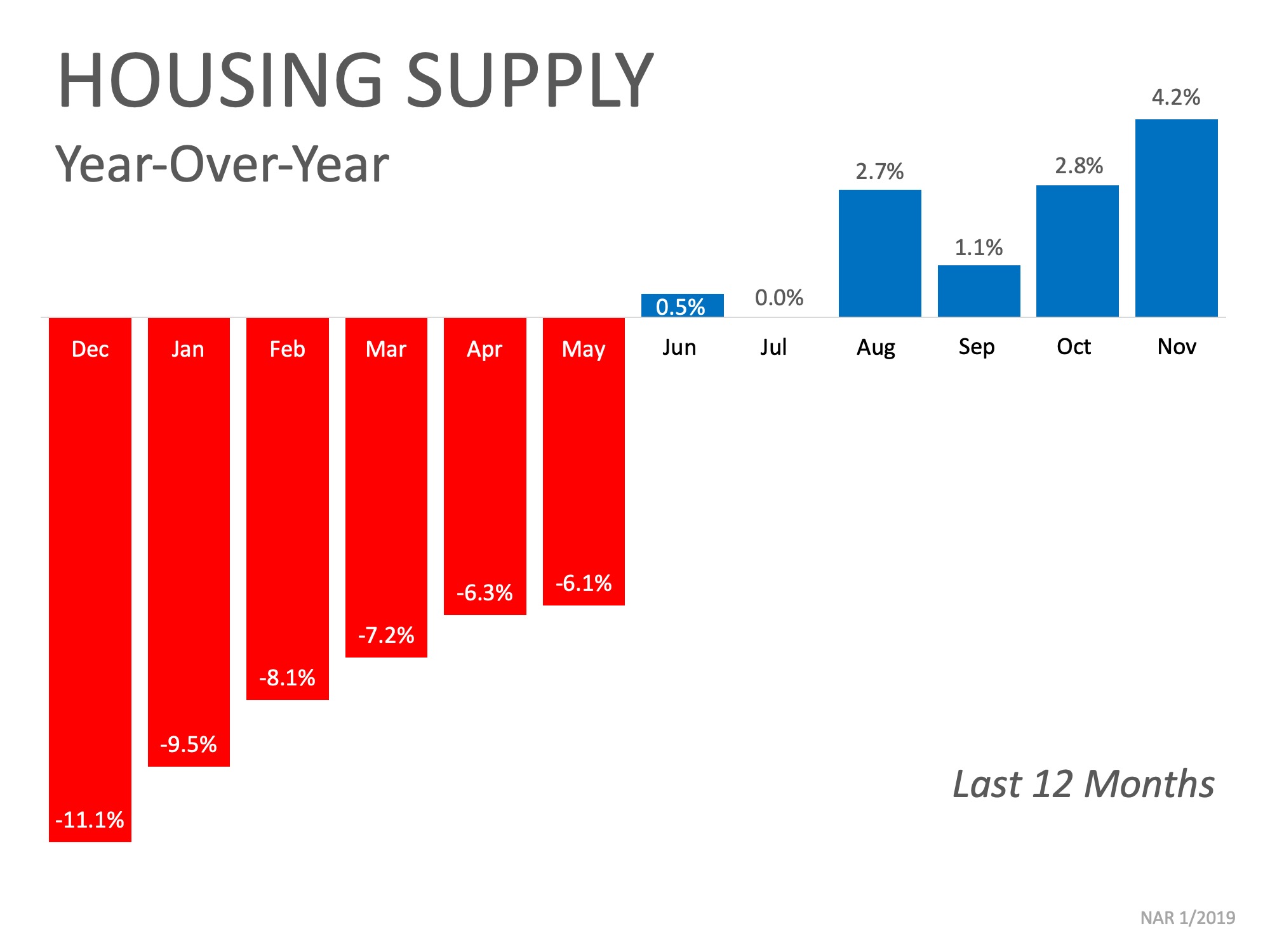

A ‘normal’ real estate market requires there to be a 6-month supply of homes for sale in order for prices to increase only with inflation. According to the National Association of Realtors (NAR), listing inventory is currently at a 3.9-month supply (still well below the 6-months needed), which has put upward pressure on home prices. Home prices have increased year-over-year for the last 81 straight months.

The inventory of homes for sale in the real estate market had been on a steady decline and experienced year-over-year drops for 36 straight months (from July 2015 to May 2018), but we are starting to see a shift in inventory over the last six months.

The chart below shows the change in housing supply over the last 12 months compared to the previous 12 months. As you can see, since June, inventory levels have started to increase as compared to the same time last year.

This is a trend to watch as we move further into the new year. If we continue to see an increase in homes for sale, we could start moving further away from a seller’s market and closer to a normal market.

If you are planning to enter the housing market, either as a buyer or a seller, let’s get together to discuss the changes in mortgage interest rates and inventory and what they could mean for you.

This year started strong for real estate, but then the market began to soften. Home inventory in the starter and move-up categories dwindled to almost nothing, mortgage rates were projected to rise, and home sales had decreased for several months in a row.

To many, the outlook heading into 2019 appeared dim… at best.

Then, in a 24-hour window last week, things seemed to change. On Wednesday, the National Association of Realtors’ (NAR) revealed in their Existing Homes Sales Report that home sales had INCREASED for the second consecutive month. The next day, NAR’s economic research team announced that the percentage of first-time buyers in the market was higher than last month and even higher than a year ago.

You only needed to wait a few hours to find out. On the heels of NAR’s revelations, Zillow released their November Real Estate Market Report that explained:

“After nearly four years of annual declines in inventory, the number of homes for sale has now increased year-over-year for three straight months…”

Ending 2018, we now know two things:

Maybe a lack of inventory was the major challenge all along.

Last Thursday (the day after all of the above news), Freddie Mac announced that mortgage rates did not increase but instead decreased…again. From their release:

“The response to the recent decline in mortgage rates is already being felt in the housing market. After declining for six consecutive months, existing home sales finally rose in October and November and are essentially at the same level as during the summer months.

This modest rebound in sales indicates that homebuyers are very sensitive to mortgage rate changes – and given the further drop in rates we’ve seen this month, we expect to see a modest rebound in home sales as well.”

Will 2019 start out better than many have predicted? Perhaps, but we’ll have to wait and see. Things do look much better today, though, than they did just a month ago.

One of the most common loans you can get to buy a home is a 30-year fixed rate mortgage. If the thought of paying for your home over the course of 30-years seems daunting, here are some easy ways to shorten that term which will actually end up saving you money over the life of your loan.

Any additional payments to the principal amount (the original sum of money borrowed in a loan), helps to cut down the amount of interest that you will pay over the life of your loan and can also help to shave years off the loan as well.

When you make ‘extra’ payments toward your loan, the key is to let your lender/bank know that you want the extra funds to go toward your principal balance as they will not automatically do this for you.

You don’t have to double your mortgage payment to make a big difference either!

If you have a 30-year mortgage on a median-priced home ($250,000) with a 5% interest rate, you’ll be responsible for a $1,342.05 monthly principal and interest payment. Over the course of the loan, if you pay your exact monthly payment, you will have paid $233,133.89 in interest alone!

Benefit: In the example above, adding $111.84 to your monthly mortgage payment might not seem like a lot, but each year you will have paid one extra month’s worth of payments which will shorten the term of your loan by 4 years and 8 months, all while saving you $42,000 in interest!

Benefit: Fifty dollars might not seem like enough to make a difference on the term of your loan, but that small amount will save you over $21,000 in interest and will take over 2 years off the end of your loan. Twenty-eight years from now, you’ll be happy to pay off your loan that much sooner!

Benefit: If you find yourself with a little extra money after a yearly bonus, a tax return, or from investment dividends, paying that money towards the principal can cut your costs. This option, however, is less predictable than the extra monthly payments.

If you have higher interest debts, like credit cards, consider using any extra funds you have to pay those debts down before applying that money towards your mortgage. Also, if you do not plan on staying in your home for more than 10 years, paying extra toward your mortgage might not make sense.

If you’re wondering what strategies would work best for you to shorten the term of your loan, let’s get together to answer your questions.