The Eastside residential market has entered a new chapter. After nearly two years of strong seller conditions, the data through March 2026 tells a clear and consistent story - the market is rebalancing. Not crashing, not stalling, but recalibrating in ways that matter whether you're buying or selling.

Here's what I'm seeing across my core markets of Bellevue, Redmond, Kirkland, Woodinville, Sammamish, Issaquah, and Bothell.

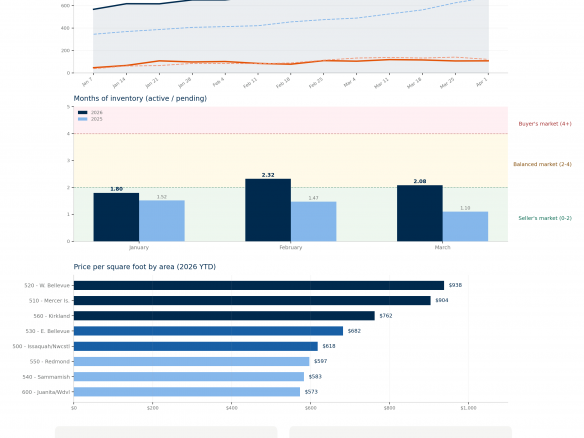

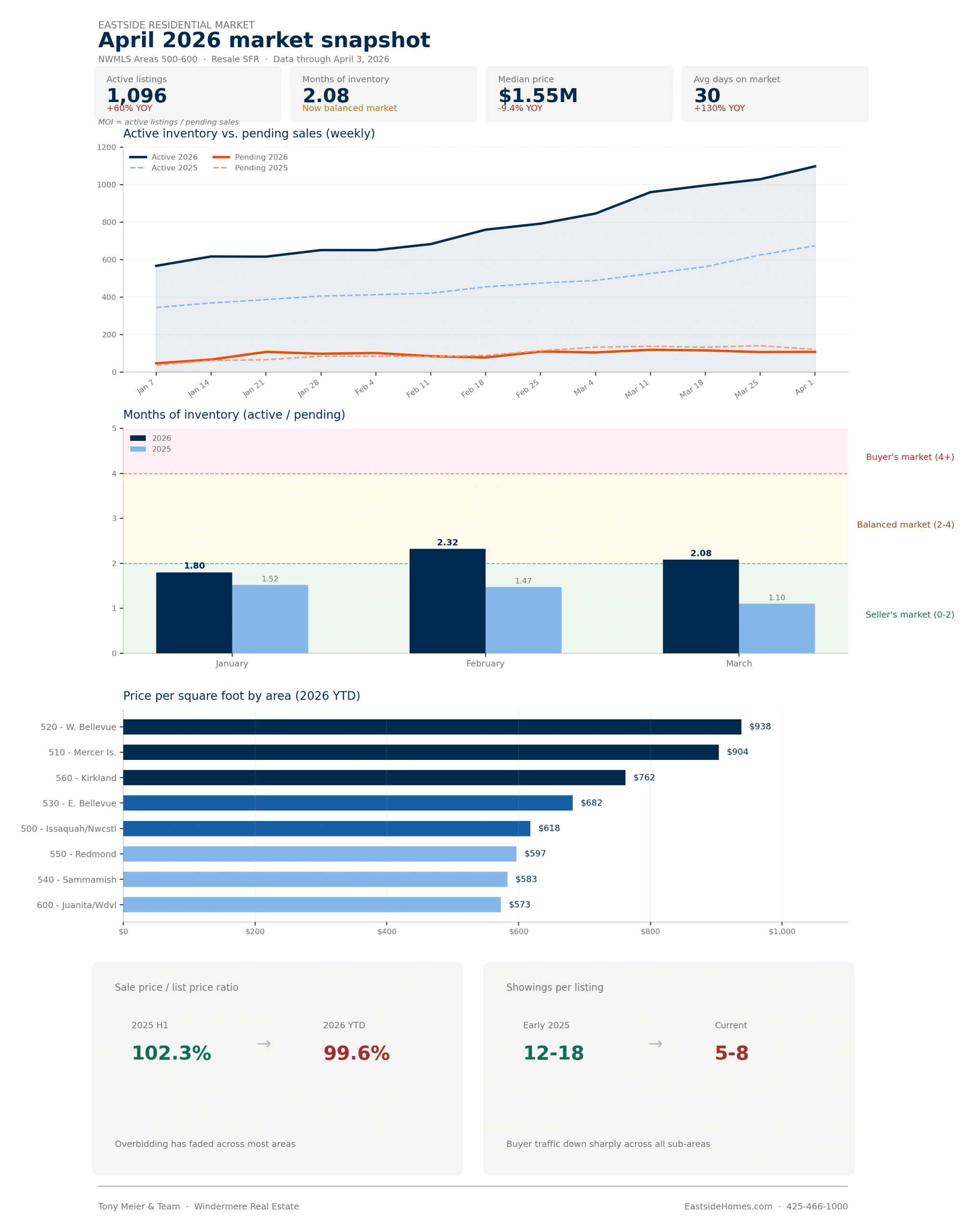

Inventory Is the Defining Story

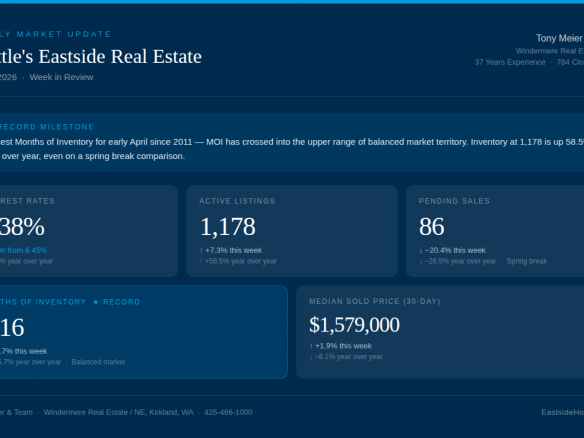

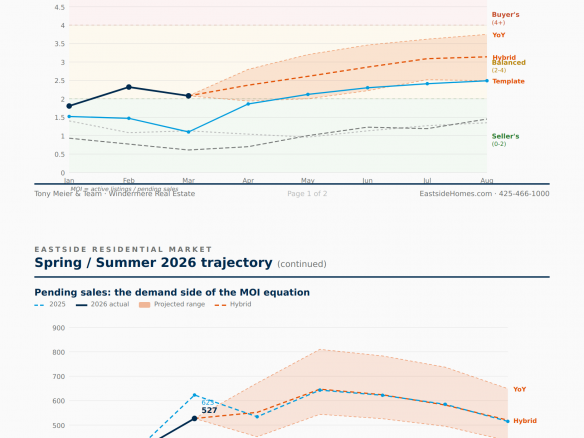

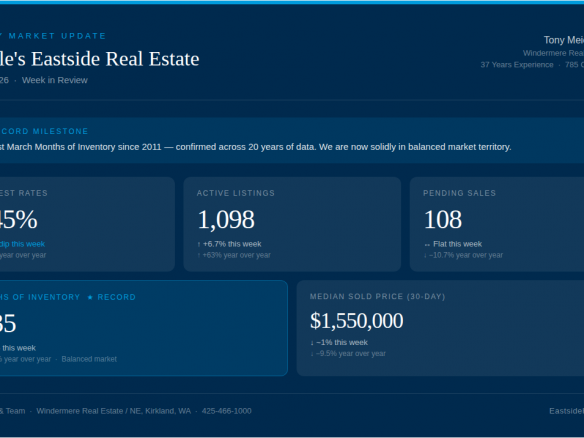

Active residential listings across the Eastside reached 1,096 in March - up 60% from 684 at the same time last year. Months of inventory (active listings divided by pending sales) has climbed to 2.08, nearly double the 1.10 from March 2025. That's significant: we've crossed out of seller's market territory (0-2 months) and into a balanced market (2-4 months) for the first time since early 2023.

The inventory build has been steady and broad-based. Every Eastside sub-market is carrying more active listings than a year ago, with some areas seeing their available homes nearly double.

Prices Have Softened - But the Story Varies by Location

The Eastside residential median came in at $1,550,000 in March, down 9.4% from $1,710,000 last March. Price per square foot across the Eastside is averaging $626 year to date, compared to $663 during the first half of 2025 - a decline of roughly 5-6%.

That said, the pressure is not evenly distributed. The Juanita and Woodinville corridor (NWMLS Area 600) has shown more resilience, with median prices down just 1.2% year over year and recent closings printing at $606 per square foot - a noticeable improvement from the $570 range late last year. Sammamish and parts of Redmond have seen steeper adjustments, with some pockets down 10-12% from their 2025 peaks.

Buyer Activity Has Slowed

Pending sales across the Eastside were down 15% in March compared to last year (527 vs. 623). Showings per listing have dropped from the 12-18 range in early 2025 to roughly 5-8 across most areas. Average days on market has more than doubled - from 13 days during the first half of 2025 to 30 days so far in 2026.

The sale price to list price ratio reflects this shift. A year ago, most Eastside areas were consistently seeing homes sell at 101-104% of list price. Today that number sits at 99-101%, meaning the competitive overbidding dynamic has largely faded.

What This Means for Sellers

Pricing accuracy has never been more important. Homes that are well-prepared, correctly priced, and strategically marketed are still moving - many within the first two weeks. But the margin for error has narrowed considerably. Overpriced properties are sitting, and the data shows 27% of closings this year had 60 or more days on market. That's a very different environment from 12 months ago.

What This Means for Buyers

You have more options, more time, and more leverage than at any point since early 2023. Inventory levels, longer days on market, and a shift toward at-or-below-list pricing all create room to be thoughtful and strategic. That said, this is still the Eastside - well-priced homes in desirable areas are generating strong interest. The key is recognizing which properties represent genuine opportunity versus those that are sitting for a reason.

Looking Ahead

It's tempting to look at recent closing data and see encouraging signs - price per square foot, days on market, and sale-to-list ratios all improved in the last two weeks of March. But closings are a lagging indicator. Those transactions reflect buyer decisions made in mid-February and early March, when mortgage rates were roughly half a point lower and active inventory was still below 850 listings. They're a snapshot of a market that has already passed.

The forward-looking indicators - weekly pending activity, showings per listing, and the pace of inventory growth - all point toward continued softening through spring and into summer. Months of inventory at 2.08 is the highest level the Eastside has seen since 2011, and the gap between active listings and pending sales continues to widen. The closings that will reflect today's market conditions won't appear in the data until late April and May.

What I can say with confidence: this market rewards preparation, accurate pricing, and deep local knowledge. The days of "list it and let the market do the work" are behind us - at least for now.

Tony Meier has 37 years of experience and 785 closed residential sales, including 208 sales in the English Hill neighborhood of Redmond - more than any other broker, team, or real estate company. Reach Tony at 425-466-1000 or visit EastsideHomes.com.