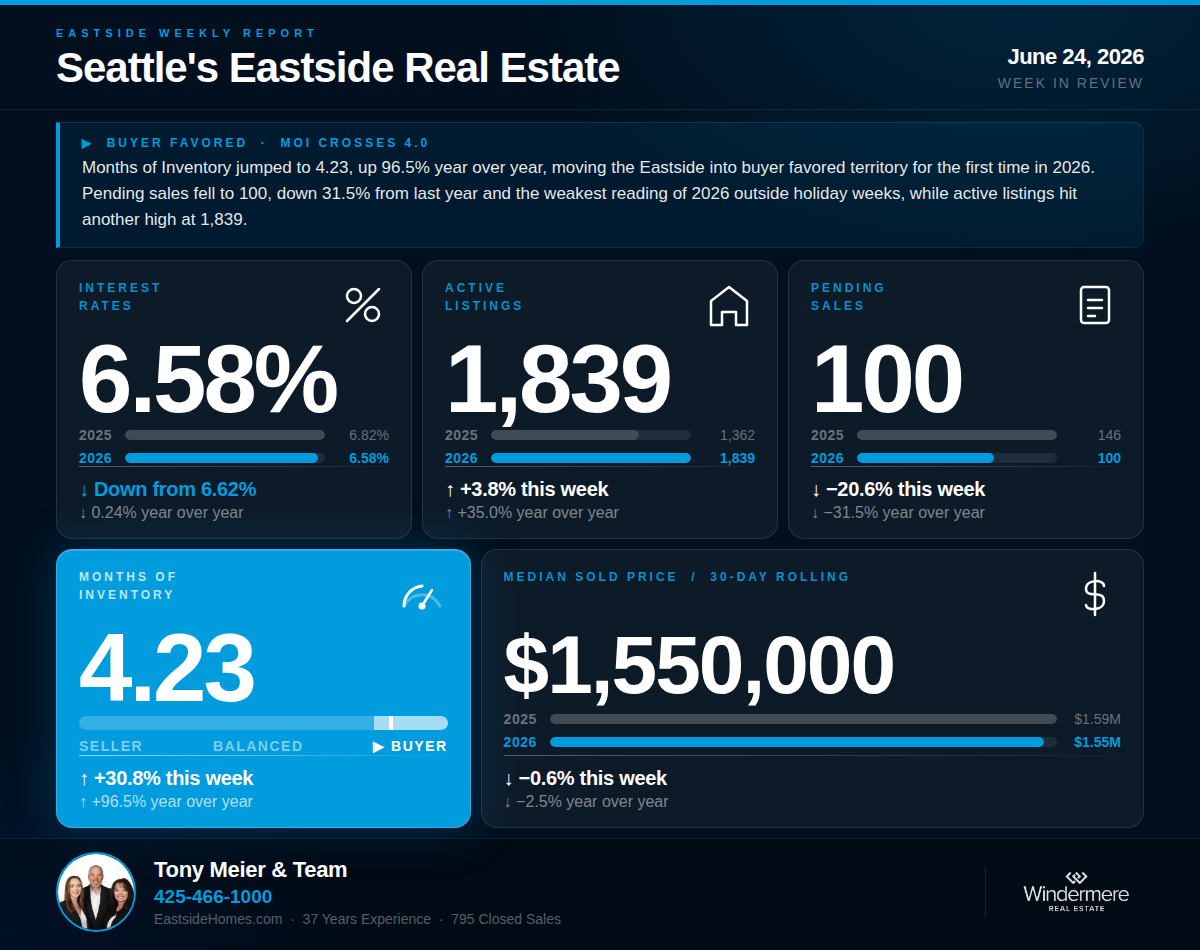

4 Min. Read

Audio Version

Tony Meier | Windermere Real Estate | 37 Years Experience | 793 Closed Eastside Sales

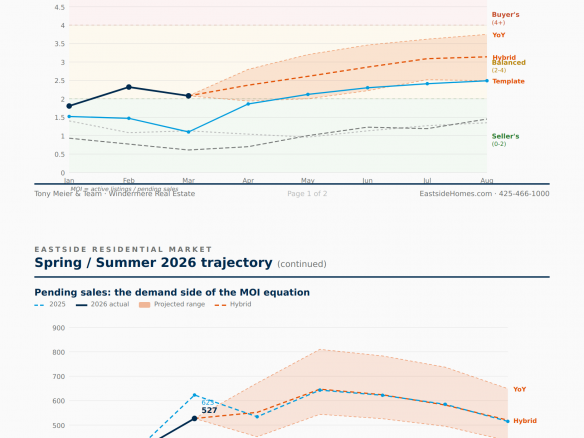

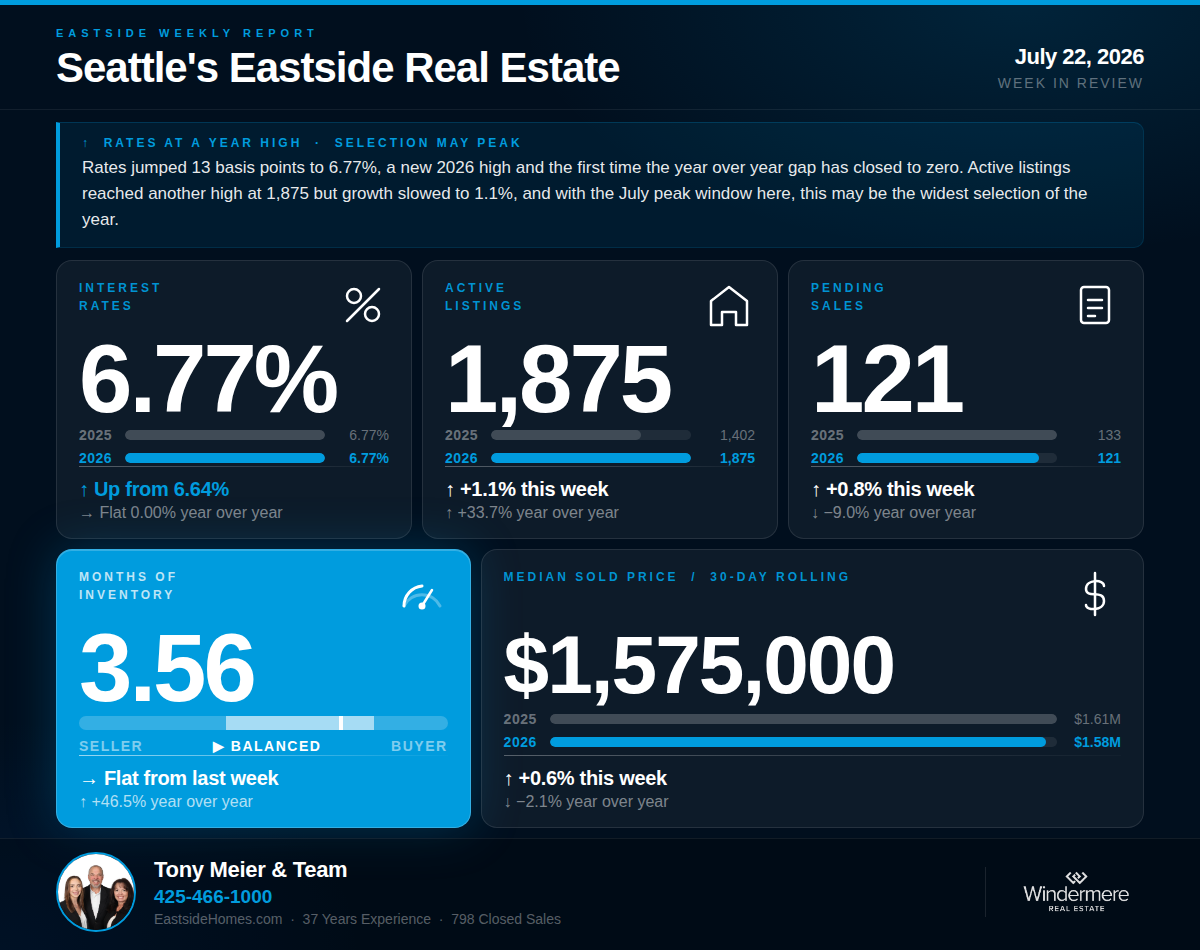

Three signals converged this week that sharpen the June picture considerably. Pending sales dropped sharply to 120 from last week's 138 — and the year-over-year comparison widened to negative 17.2%, the largest YOY pending gap in months. Rates returned to the post-conflict high of 6.67%. And Months of Inventory jumped back to 3.34 — the second-highest weekly reading of 2026, this time without any holiday distortion to explain it.

💰 Interest Rates — 6.67%

↑ Up from last week's 6.61% | ↓ Down 0.26% year over year

Rates climbed back to 6.67% this week — up six basis points from last week and matching the post-conflict high recorded three weeks ago on May 20. The pre-conflict baseline of 5.99% is now 0.68 points below where rates sit today. Year over year, rates remain down 0.26%, but the YOY tailwind has narrowed compared to earlier in 2026 as the comparison base from 2025 declines. On a $1.5M home, this week's rate still represents roughly $680 more per month in carrying costs than buyers faced in late February.

🏡 Active Listings — 1,745

↑ Up 3.1% from last week | ↑ Up 29.9% year over year

Active listings reached 1,745 this week — another 2026 high and up 29.9% from the 1,343 homes on the market during the comparable week in 2025. The inventory build continues at its steady pace, adding 53 listings net over the past week as we move closer to the historical July peak.

📝 Pending Sales — 120

↓ Down 13.0% from last week | ↓ Down 17.2% year over year

Pending sales fell sharply to 120 this week — down 13.0% from last week's 138 and the lowest non-holiday reading since April. Year over year, pending is now down 17.2% from the 145 recorded during the comparable week in 2025. This is the widest YOY demand gap in 2026 outside of the Memorial Day distortion. Two consecutive weeks of June data now show pending running 8% and 17% below 2025 respectively — the seasonal decline we anticipated is accelerating, and it is happening from a demand base that was already weaker than last year.

📦 Months of Inventory — 3.34

↑ Up 18.6% from last week's 2.82 | ↑ Up 56.5% year over year

MOI jumped to 3.34 this week — up 18.6% from last week and 56.5% above the 2.14 recorded during the comparable week in 2025. Two weeks ago, Memorial Day temporarily pushed MOI to 3.38. This week's reading of 3.34 is essentially the same level without the holiday explanation — a meaningful signal. MOI remains in balanced market territory, defined locally as 2 to 4 months, but is now solidly in the upper half of that range with buyer-favored conditions (4+ months) within reach if current weekly patterns continue.

🏠 Median Sold Price (Rolling 30-Day) — $1,550,000

↑ Up 1.8% from last week | ↓ Down 7.7% year over year

The 30-day median ticked up modestly to $1,550,000 — up 1.8% from last week, the first week-over-week gain in several weeks. Year over year, the 30-day median remains 7.7% below the $1,680,000 recorded at this same point in 2025. Closed sales came in at 103 — down 2.8% year over year from the 106 recorded during the comparable week in 2025.

🔍 The Big Picture — What This All Means

The story this week is the convergence of three signals pointing in the same direction. Demand is weakening on schedule with the seasonal pattern, but from a starting point that was already 8% below last year. Inventory continues to grow as we approach the July peak. Rates have returned to their post-conflict high, removing the modest tailwind that briefly emerged. MOI has reached a non-holiday level that matches the Memorial Day reading — confirming that the structural conditions defining 2026 are intensifying as the season progresses. None of this is a crisis. What it is, is a market that has now spent four consecutive months operating under measurably tighter conditions for sellers than at any point since 2011 — and the seasonal pattern suggests those conditions will continue to firm through summer.

🏠 For Sellers

With 29.9% more competition on the market than a year ago and pending demand 17% below last year's comparable week, pricing discipline is more critical now than at any point in 2026. The seasonal decline in buyer activity is underway and accelerating. Inventory will continue building toward the July peak while pending sales decline further from the May high. Sellers who are in the market now with accurate pricing are competing in a better environment than those who wait through summer.

We have done extensive analysis on what this shift means for sellers in each Eastside sub-market and would welcome the opportunity to walk you through what the data shows for your specific area and home.

🔑 For Buyers

Buyers today have more negotiating leverage for this time of year than at any point since 2011. Active listings are still growing toward the historical July peak, meaning the widest selection window of 2026 remains ahead for prepared buyers. With rates back at the post-conflict high of 6.67%, stress-testing your qualification at current levels before making a move is more important than ever. Well-priced homes are still moving — but the buyer pool is smaller and more selective than at any spring in over a decade.

If we can help you think through what this means for your move, we are here.

Tony Meier & Team — Windermere Real Estate / NE, Kirkland, WA