5 Min. Read

Audio Version

[audio mp3="https://eastsidehomes.com/wp-content/uploads/Eastside-Real-Estate-Market-Update-7-8-26.mp3"][/audio]

Tony Meier | Windermere Real Estate | 37 Years Experience | 796 Closed Eastside Sales

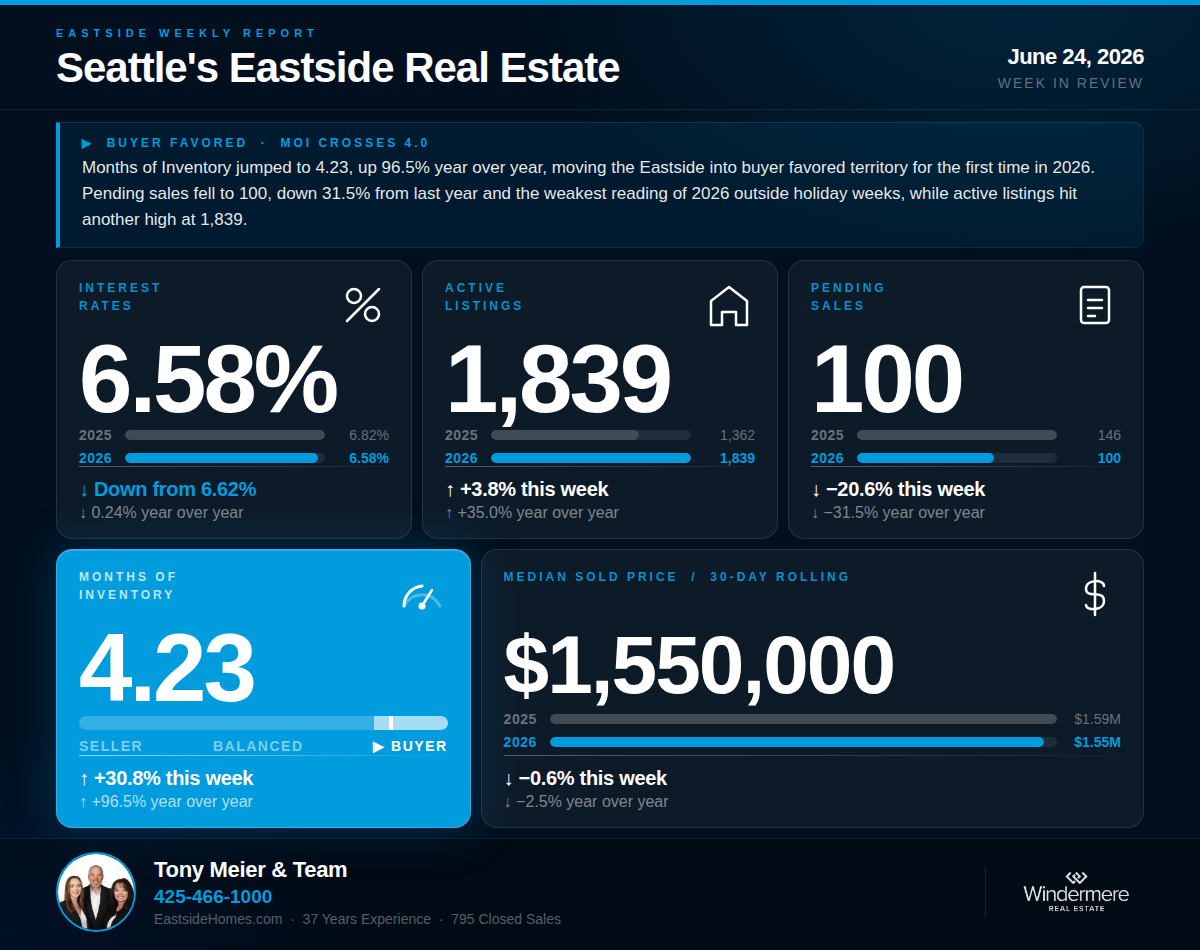

This week's headline numbers are the most extreme readings of 2026, but they arrive with the Independence Day holiday firmly stamped on them and must be read accordingly. Pending sales dropped to 72, Months of Inventory jumped to 5.78, and active listings declined for the first time all year. Before drawing structural conclusions, holiday context is essential. Last week we noted that the pre-holiday pending surge to 137 would likely reverse this week, similar to what we saw around Memorial Day when pending fell to 113. This week's 72 is that reversal, and then some. A clean read of underlying market conditions will not be available until next week's data arrives.

Updated Kirkland Rambler: 3 Beds, 1.75 Baths, Lake Washington Schools

12845 109th Ave NE, Kirkland Details

3 weeks ago

PENDING! Move-In Ready Condo in Lake Stevens: New Flooring, Updated Baths, Attached Garage

8916 Meridian Pl NE Unit A201, Lake Stevens Details

4 weeks ago

SOLD! Fully Updated 3 Bedroom Two Story Redmond Home with Modern Finishes & Sunny West-Facing Backyard

13505 174th Ave NE, Redmond Details

2 months ago

SOLD! English Hill Two-Story in Redmond. Main-Floor Guest Bedrooms, Versatile Loft, New Roof, One Block to Awarding Winning Sunrise Elementary

13831 173rd Ave NE, Redmond Details

3 months ago

SOLD! Echo Lake Retreat in Snohomish on 4.59 Acres: 4 Beds, 3.5 Baths, Chef’s Kitchen, Home Theater, & Lower Level Built for Entertainment

14425 235th St SE, Snohomish Details

3 months ago

SOLD! Coventry on English Hill in Redmond — Updated Kitchen and Stunning Primary Bath, Private Fenced Yard, Northshore School District

14151 174th Pl NE, Redmond Details

3 months ago

SOLD! Rambler on Cul-de-Sac Backing to Greenbelt on English Hill: New Kitchen, Updated Roof, A/C, 3 Bed, 1.75 Bath, No HOA

17718 NE 137th Ct, Redmond Details

3 months ago

SOLD! Private Acreage Log Home in Woodinville, 3 Bedrooms, 3 Baths, Two Brick Fireplaces, Detached 2-Car Garage with Shop, No HOA

18020 214th Ave NE, Woodinville Details

3 months ago

SOLD! Updated English Hill Home with Remodeled Baths, Flexible Floor Plan Including a Den and Rec Room, Completed by a Private Evergreen Backyard

13515 173rd Pl NE, Redmond Details

4 months ago

This week's headline numbers are the most extreme readings of 2026, but they arrive with the Independence Day holiday firmly stamped on them. Pending fell to 72, MOI jumped to 5.78, and active listings declined for the first time all year. A clean read of underlying market conditions will not be available until next week.

Pending sales jumped 37% this week to 137, MOI pulled back to 3.10 returning to balanced territory, and active listings barely grew for the first time all year. But pre-holiday timing complicates the read, and next week's Independence Day suppression is likely to reverse the pending signal.

4 Min. Read Audio Version Tony Meier | Windermere Real Estate | 37 Years Experience | 795...

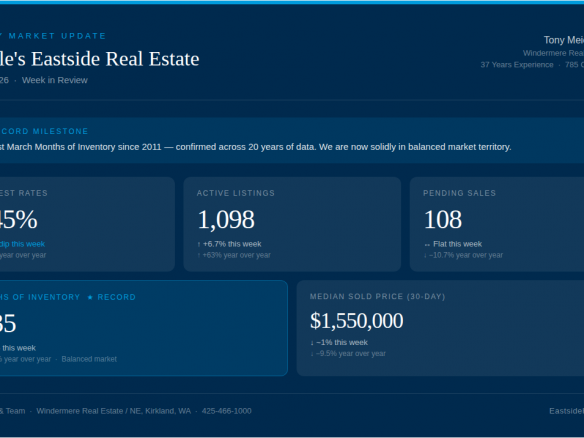

The data this week reads in mixed directions: rates eased to 6.62%, pending sales firmed modestly to 126, and active listings climbed to 1,771 — another 2026 high. Four short-term signals moved in sellers' favor this week, but the structural conditions defining 2026 remain in place.

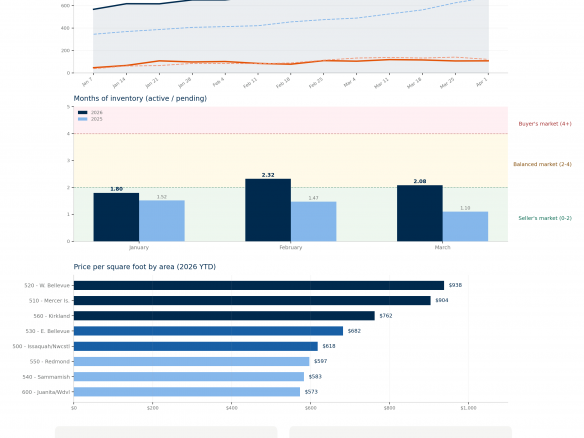

Three signals converged this week: pending sales fell sharply with the YOY gap widening to -17.2%, rates returned to the post-conflict high of 6.67%, and Months of Inventory jumped to 3.34 — the second-highest weekly reading of 2026, this time without holiday distortion to explain it.

Published on: June 3, 2026 Northwest Multiple Listing Service (NWMLS), the source for the most...

Tony Meier & Team's Weekly Market Update 4 Min. Read Audio Version 🏡 June...

Tony Meier & Team's Weekly Market Update 4 Min. Read Audio Version 🏡 May Is...

Tony Meier & Team's Weekly Market Update 5 Min. Read Audio version 🏡 A New...

Published on: May 5, 2026 Northwest Multiple Listing Service (NWMLS), the source for the most...

Tony Meier & Team's Weekly Market Update 5 Min. Read Audio Edition: 🏡...

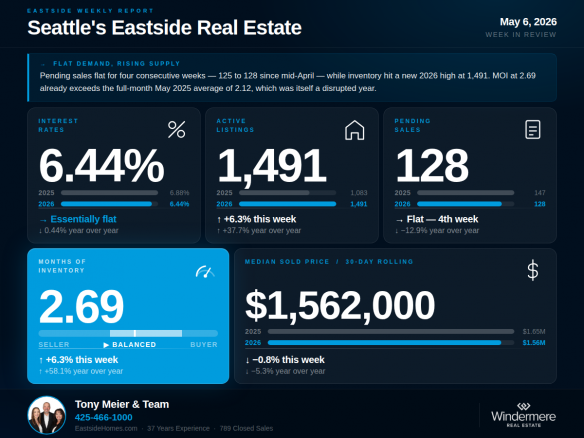

Tony Meier & Team's Weekly Market Update 3 Min. Read 🏡 Flat Demand, Rising...

Tony Meier & Team's Weekly Market Update 4 Min. Read Audio version: 🏡 April...

Tony Meier | Windermere Real Estate | 37 Years Experience | 788 Closed Eastside Sales Audio...

Tony Meier | Windermere Real Estate | 37 Years Experience | 788 Closed Eastside Sales Audio...

If you've been watching the Puget Sound real estate market and wondering what's really going on...

Tony Meier | Windermere Real Estate | 37 Years Experience | 785 Closed Sales Audio Version...

Published on: April 2, 2026 Northwest Multiple Listing Service (NWMLS), the source for the most...

There's a natural tendency in real estate to look at recent closings and draw conclusions...

The Eastside residential market has entered a new chapter. After nearly two years of strong seller...

Tony Meier & Team's Weekly Market Update 4 Min. Read. Audio Format Here: 🏡...

Published on: March 4, 2026 Northwest Multiple Listing Service (NWMLS), the source for the most...

Published on: February 4, 2026 Northwest Multiple Listing Service (NWMLS), the source for the...

Published on: January 6, 2026 Northwest Multiple Listing Service (NWMLS), the source for the most...

3 Fed Rate Cuts... Mortgage Rates Don't Budge! Seattle's Eastside Real Estate Update •...

Published on: November 5, 2025 Northwest Multiple Listing Service (NWMLS), the source for the...

Published on: October 6, 2025 Northwest Multiple Listing Service (NWMLS), the source for...

Published on: September 4, 2025 Northwest Multiple Listing Service (NWMLS), the source for...

This analysis of the Western Washington real estate market is provided by Windermere Real...

If you've ever dreamed of buying your own place, or selling your current house to upgrade,...

Sunrise sellers Shilpa Nagde and Anurag Gomsale share their experience working with Tony Meier & Team.

We had an exceptional experience working with Tony Meier and team, and we couldn't be happier with...

When it was time to sell my house I decided to have Tony Meier and his team help me because many of...

I've worked with Tony on buying two houses and selling one. I've also worked with Tony when...

Thanks to Tony Meier & Team, we found our dream property in a great location! Then, with...

We had a fantastic experience working with Tony to sell our home. From the very beginning, Tony...

Tony is a consummate professional. If you want to sell your house quickly and at the maximum...

We had the pleasure of working with Tony and his team to sell our home in English Hill, and we...

I can hardly think of more demanding customers than the two of us, but Tony rose up to the...

Tony was exceptional in assisting us in the sale of our home in a very difficult market. He helped...

Tony Meier has represented us as both a buyer and a seller in English Hill this year. As we...

For over 20 years, Tony, Wendi, and Rachel have been our trusted friends and neighbors—but...

I had the pleasure of working with Tony Meier to sell my English Hill home. Tony took the time...

Thank you so much for all your help and support in the home buying process. Your care, kindness...

Thank you for the team ! "Excellent reputation in the real estate business, reliability and...

Selling our home in English Hill was a major milestone, and we couldn’t be happier that we...

We have used Tony Meier for two home purchases, and one home sale (and currently working with him...

“Tony and team made our first home buying experience extremely smooth and stress free. His...

"Tony and his team are amazing. Trust what he tells you and do what he says. We did the changes/...

"Tony Meier and Team were extremely helpful in selling our home quickly and efficiently within a...

"It's never easy to say goodbye to a house full of memories and a neighborhood you love. But when...

"My husband Rob and I have always known we would use Tony & his team when the time came to sell...

"We are thrilled to express our gratitude to Tony for his exceptional guidance in our first home...

"Tony and Team provided us with resources and support for a smooth and pleasant property sale of...

"Tony and his team made the process of selling our house as easy as it could possibly be. He had...

"Tony and his team did an amazing job in helping us sell our home. Tony has a deep understanding of...

"On my visits to the area, I've seen your name for the last dozen years or so. Really good to...

We were grateful for the guidance provided by Tony Meier & Team to help us navigate the selling...

My father’s condo needed to be sold quickly. I hesitated reaching out to Tony out to due to the...

"Tony and his team made the sale of my English Hill home a smooth process. Having lived in the...

Compare listings

Compare